Introduction to Elasticity of Demand

Elasticity of demand is an important concept in economics, because it measures how responsive consumers are to changes in prices. Elasticity of demand is the degree to which a given quantity of a good or service can be produced in response to changes in the price of that good or service.

It is the tendency for the quantity demanded to vary in response to changes in price. This means that a change in price can cause a change in quantity demanded.

The elasticity of demand for a product or service can be positive, negative, or zero. If a firm’s elasticity of demand is positive, it means that it can increase production as the market demands more and vice versa. If the elasticity is negative, then it means that as the market demands less, production will also reduce and vice versa if it’s zero then there will be no change in production levels.

Elastic Demand: In elastic demand, a small change in price can lead to a significant change in quantity demanded.

Inelastic Demand: In inelastic demand, a big change in price can lead to a small or insignificant change in the demand.

Mathematical Equation for “ Elasticity of Demand ”

The price elasticity of demand is calculated as the percentage change in quantity divided by the percentage change in price.

Elasticity of Demand = Percentage change in Quantity/Percentage change in Price

e(D) = (dQ/Q)/(dP/P)

e(D)= Elasticity of Demand

d(Q)= Change in Demand

d(P)= Change in Price

Q= Quantity of Demanded Good

P= Price of Demanded Good

Types of Elasticity of Demand

There are three types of Elasticity of Demand :

- Price Elasticity of Demand

- Income Elasticity of Demand

- Cross Elasticity of Demand

Price Elasticity of Demand

Price elasticity of demand refers to the responsiveness of the quantity demanded of a good or service to a change in its price. This can be calculated as the percentage change in quantity demanded divided by percentage change in price. It is also known as responsiveness to price change.

The higher the price elasticity, the more responsive consumers are to price changes and vice versa.

Price Elasticity = Proportionate change in quantity demanded/Proportionate change in price

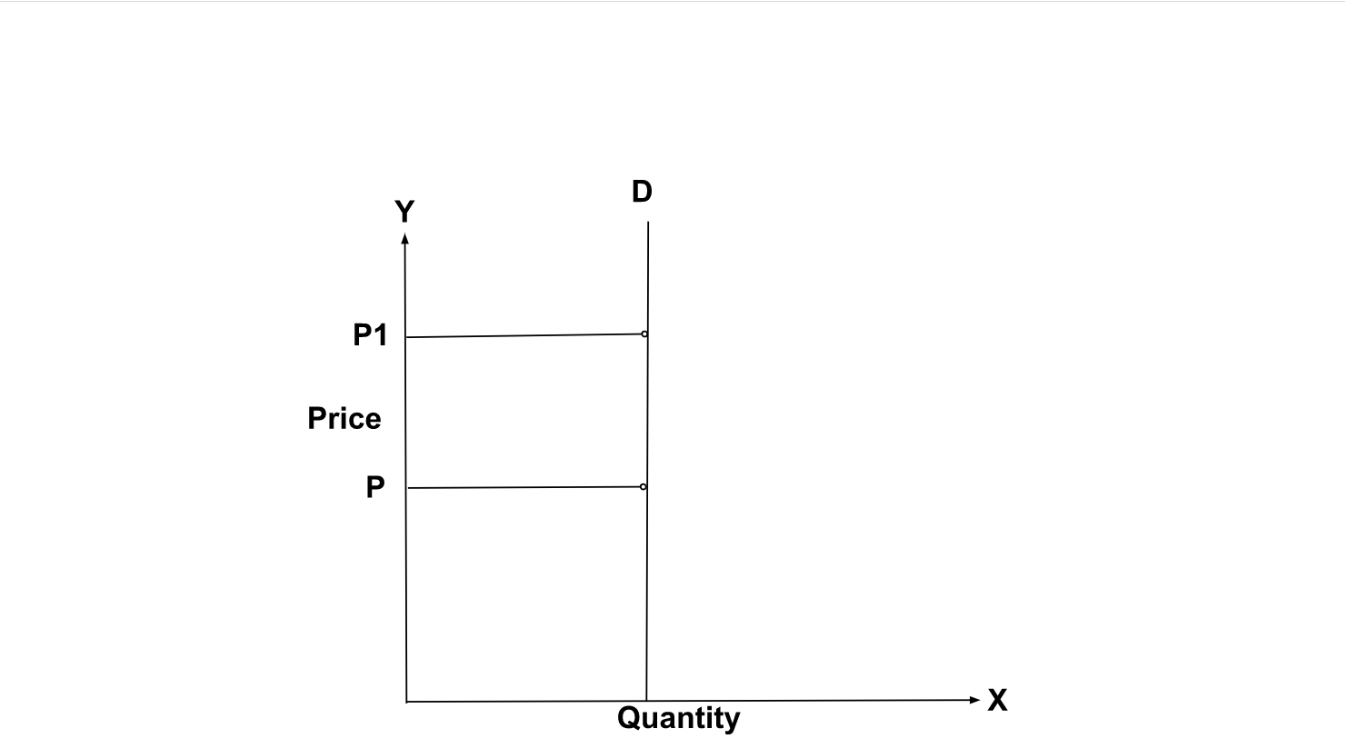

Case 1: Perfectly Elastic Demand

When a small change in price leads to an infinitely large change in quantity demanded, it is called perfectly or infinitely elastic demand. Here E=∞

Case 2: Perfectly Inelastic Demand

When even a large change in price does not impact the quantity demanded, it is perfectly inelastic demand. Here, E = 0

Case 3: Relatively Elastic Demand

When change in demand is more than the proportionate change in price, then it is considered as a relatively elastic demand i.e. a small change in price leads to a very big change in demand. Here, E > 1

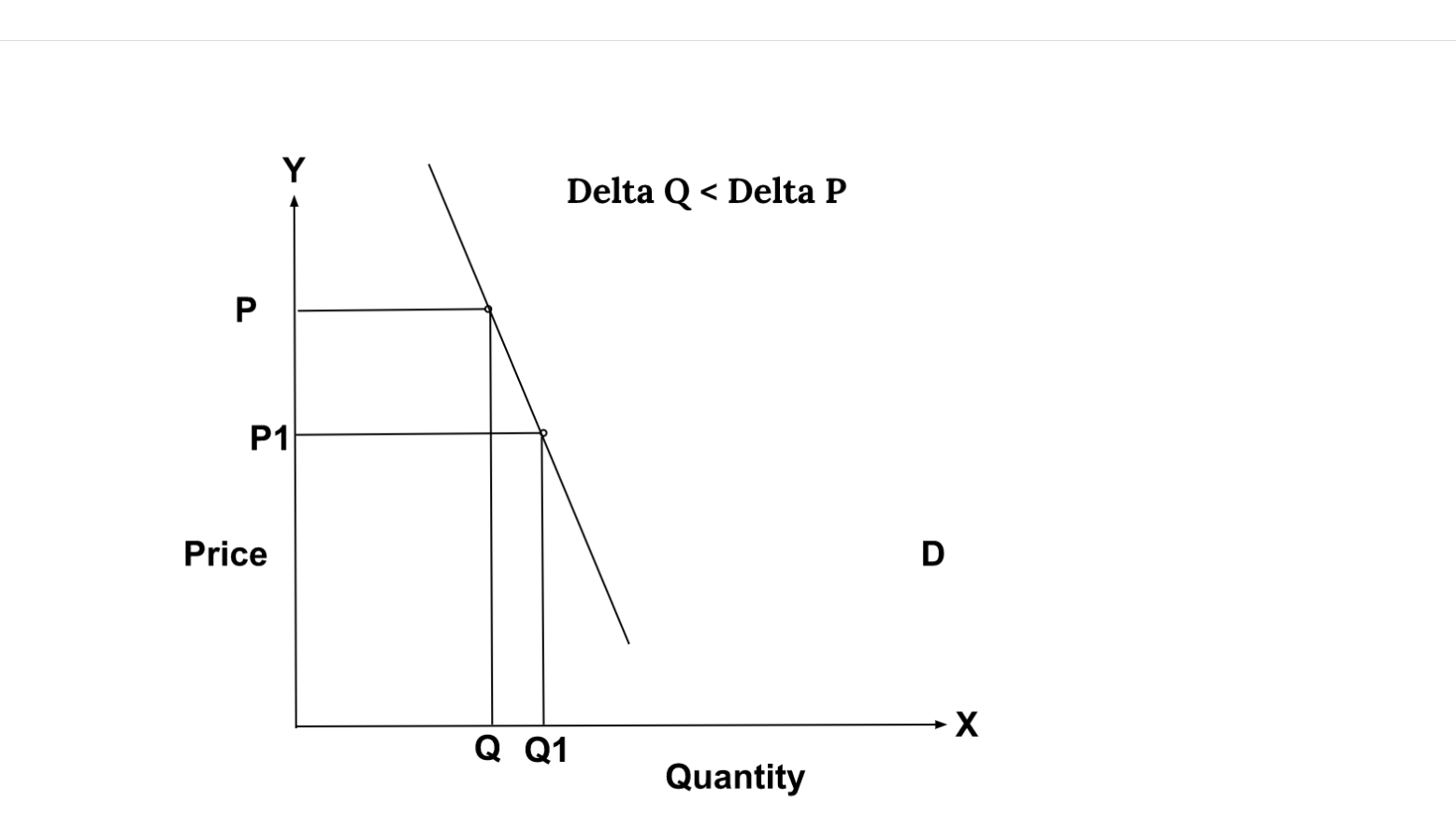

Case 4: Relatively Inelastic Demand

When change in demand is less than the proportional change in the price, such demand is relatively inelastic demand i.e. A large change in price leads to a small change in demand. Here, E < 1

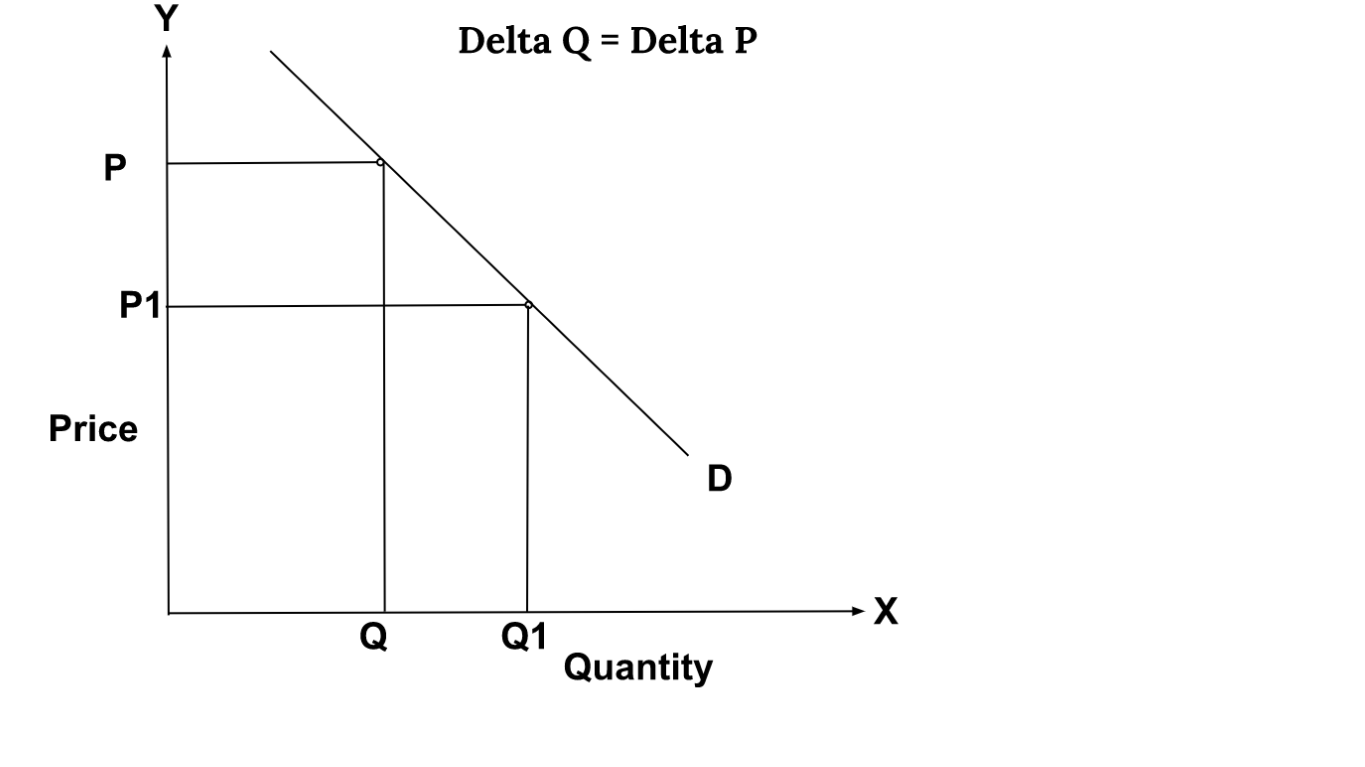

Case 5: Unit Elasticity of Demand

It is the condition when the change in demand is exactly equal to the change in price. Here, E=1

Income Elasticity of Demand

This refers to the responsiveness of the quantity demanded of a good or service to a change in its income. This can be calculated as the percentage change in quantity demanded divided by percentage change in income.

Income Elasticity = Proportionate change in quantity demanded/Proportionate change in income

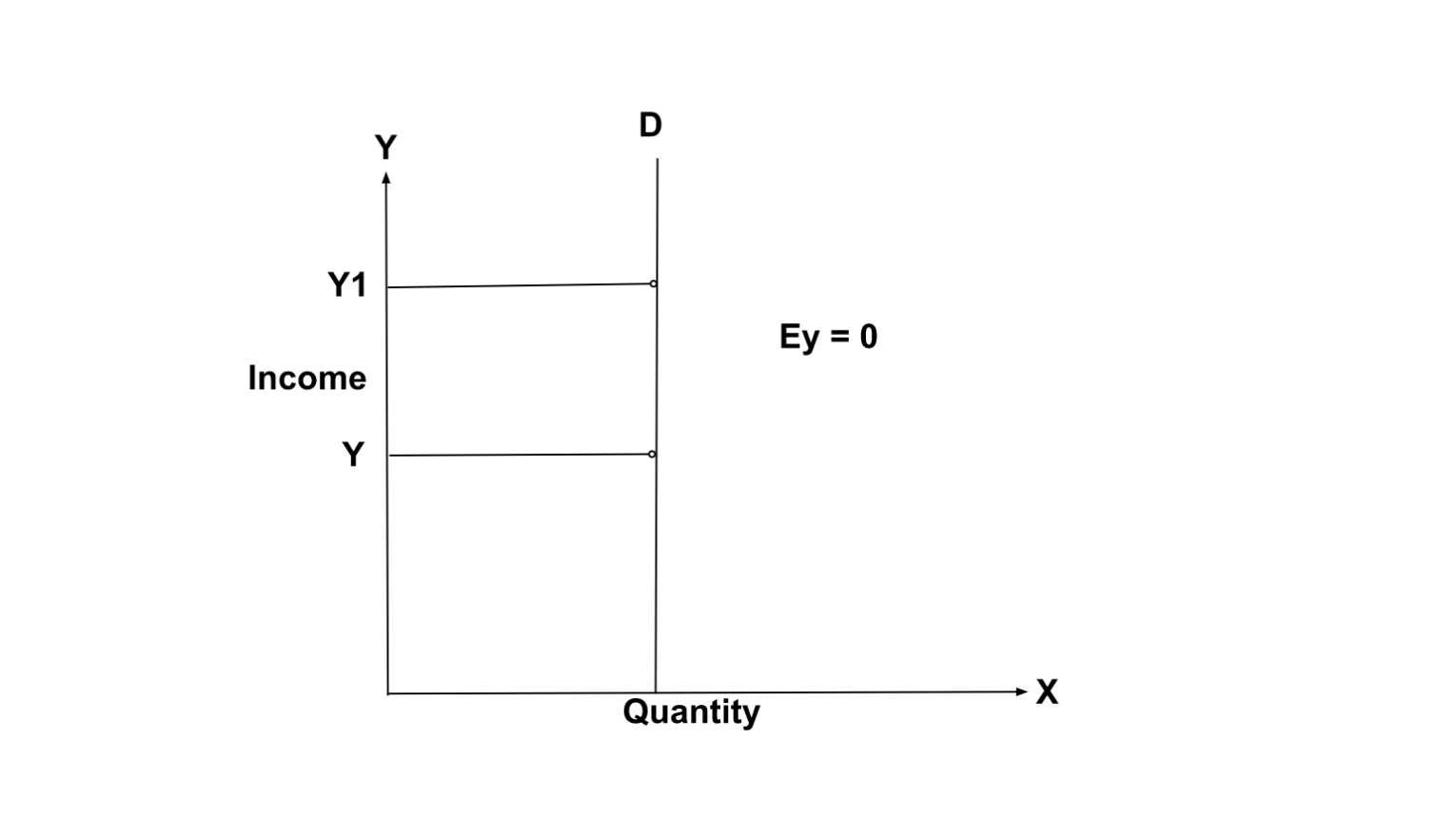

Case 1: Zero Income Elasticity

When even a large change in money income does not impact the quantity demanded, it is perfectly inelastic demand. Here, Ey = 0

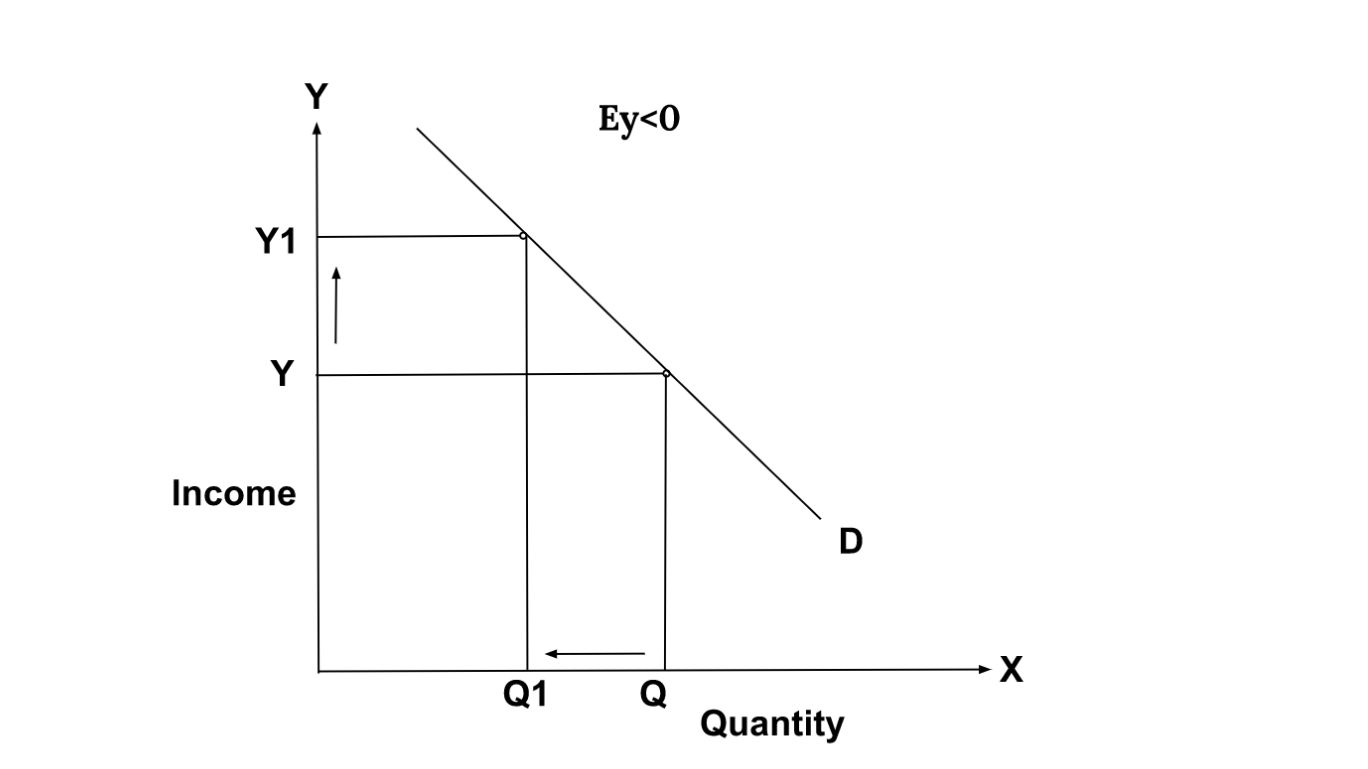

Case 2: Negative Income Elasticity

When income increases, quantity demanded falls. In this case, income elasticity of demand is negative. Here, Ey < 0

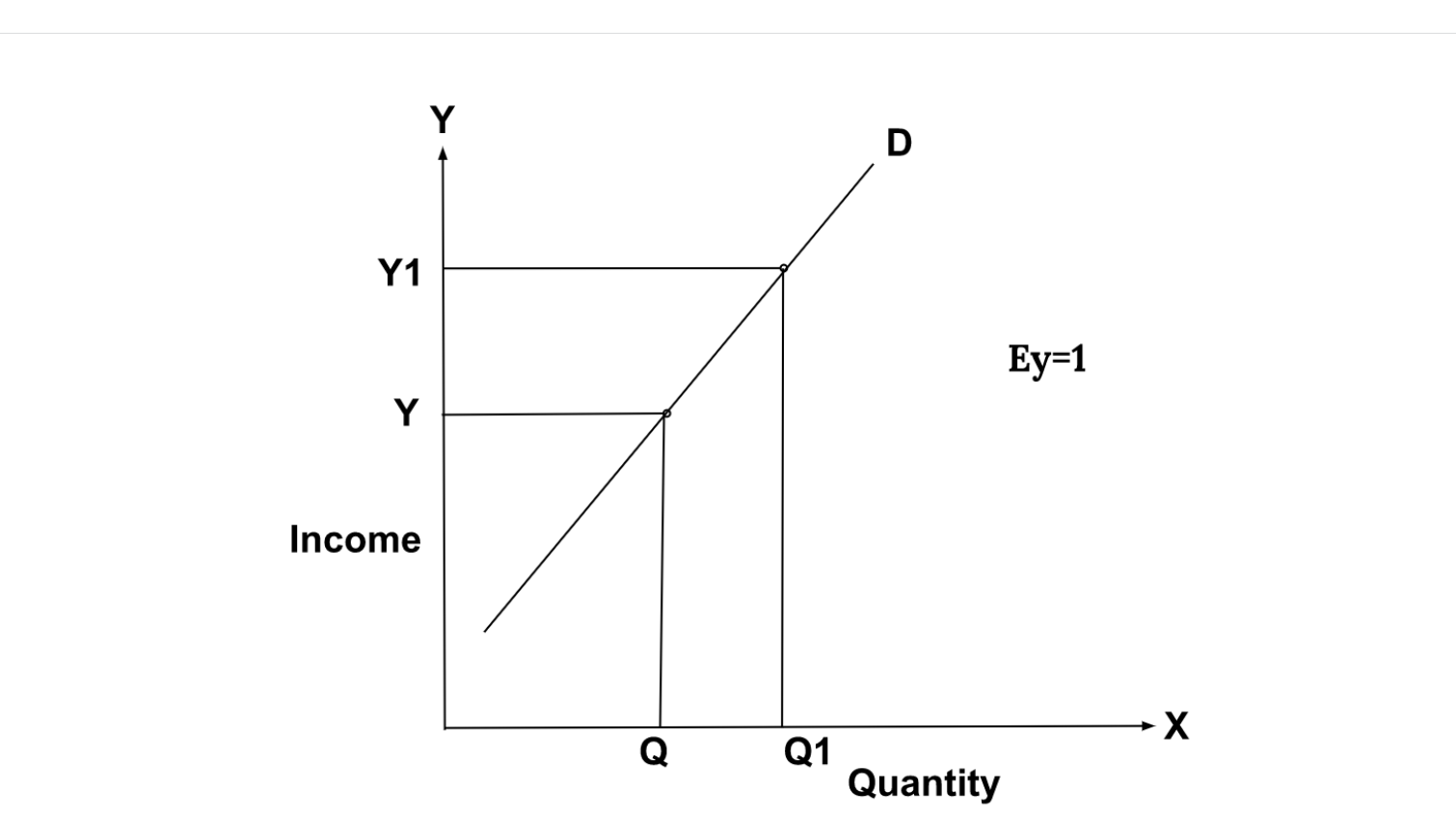

Case 3: Unit Income Elasticity

When an increase in income brings about a proportionate increase in quantity demanded, it is unit income elasticity. Here, Ey = 1

Case 4: Income elasticity greater than unity

When an increase in income brings about a more than proportionate increase in quantity demanded. Here, Ey > 1

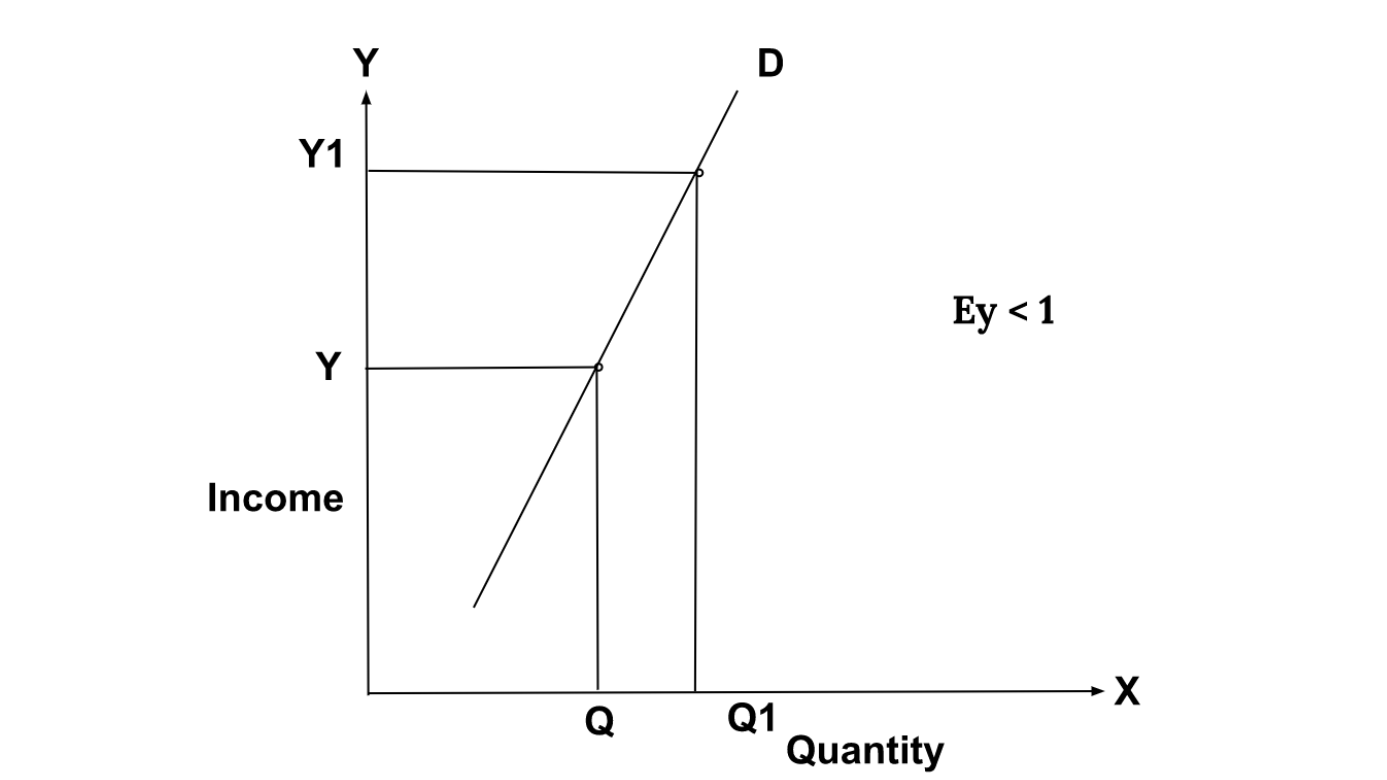

Case 5: Income elasticity less than unity

When increase in income increases the quantity demanded but less proportionately. Here, E < 1

Cross Elasticity of Demand

Cross elasticity of demand is a measure of how sensitive demand for one good is to changes in the price of another. It is calculated by the following formula:

Cross Elasticity = Proportionate change in quantity demanded of X/Proportionate change in income Y

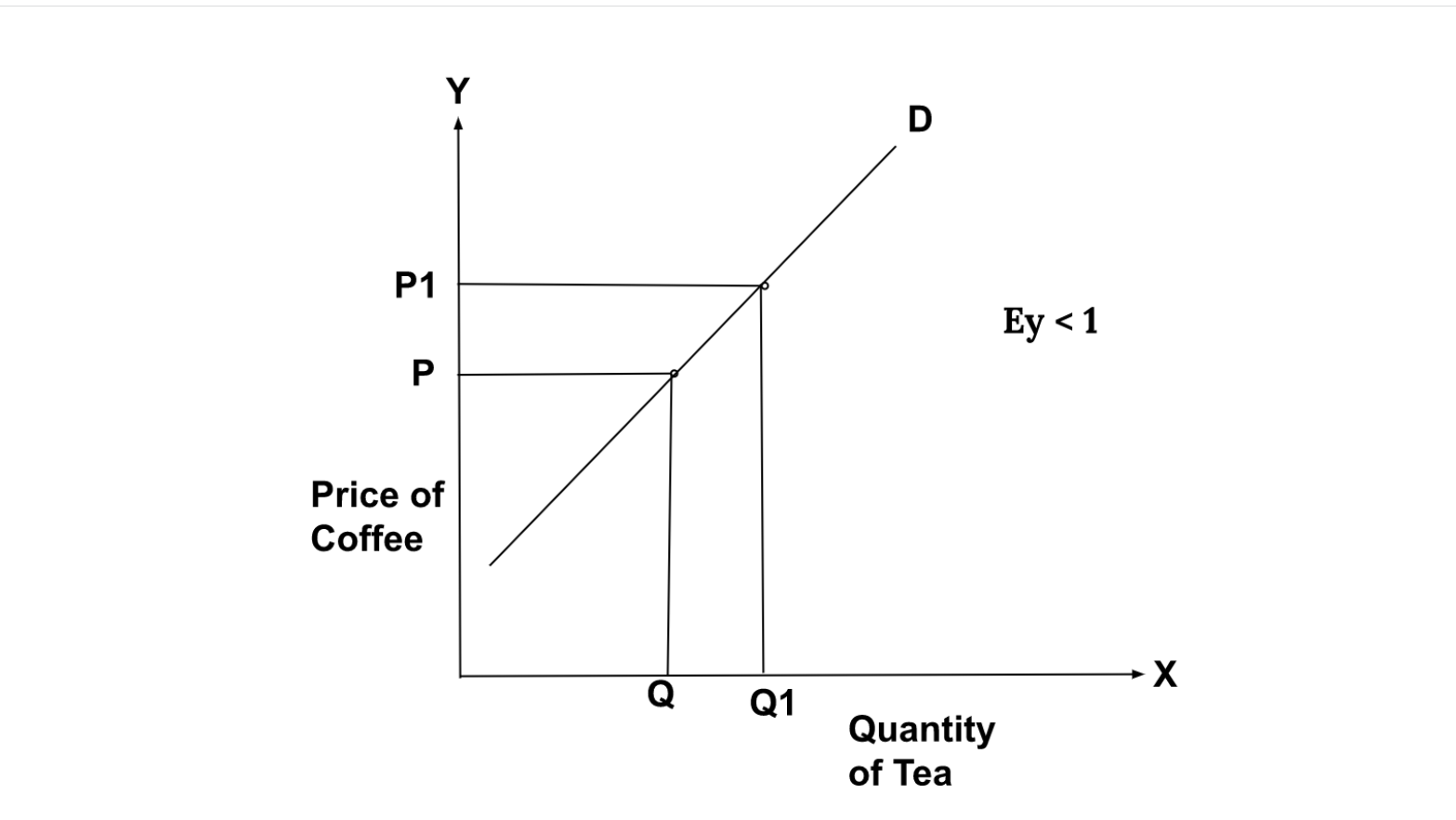

Case 1 : Cross Elasticity in Substitute Goods (Coffee and Tea)

When the price of coffee increases, the quantity demanded of tea increases. Tea and coffee are substitute goods.

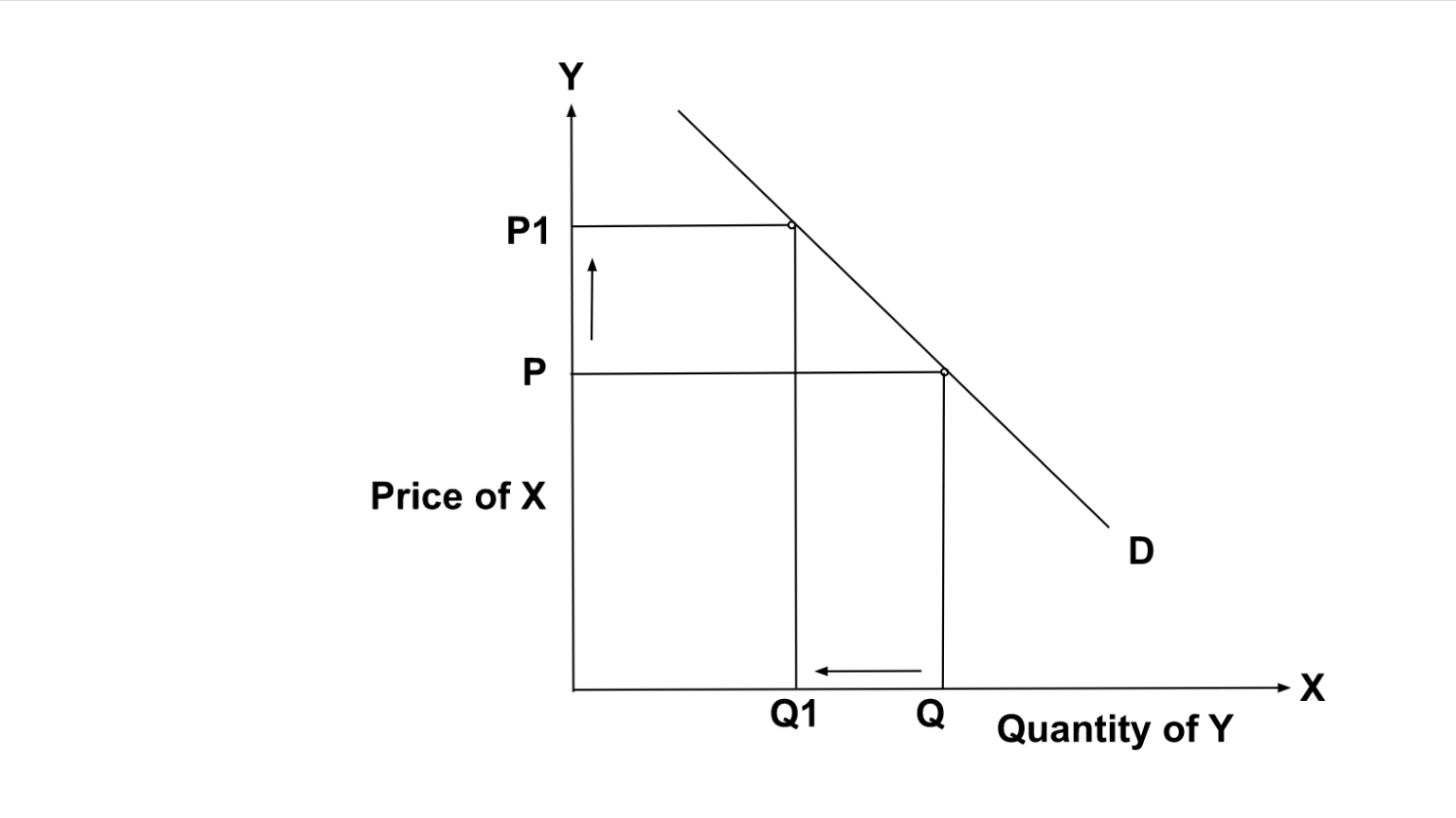

Case 2 : Cross Elasticity in Complements

Cross elasticity of complements is negative. When the increase in price of one commodity X leads to decrease in quantity demanded Y and vice versa.

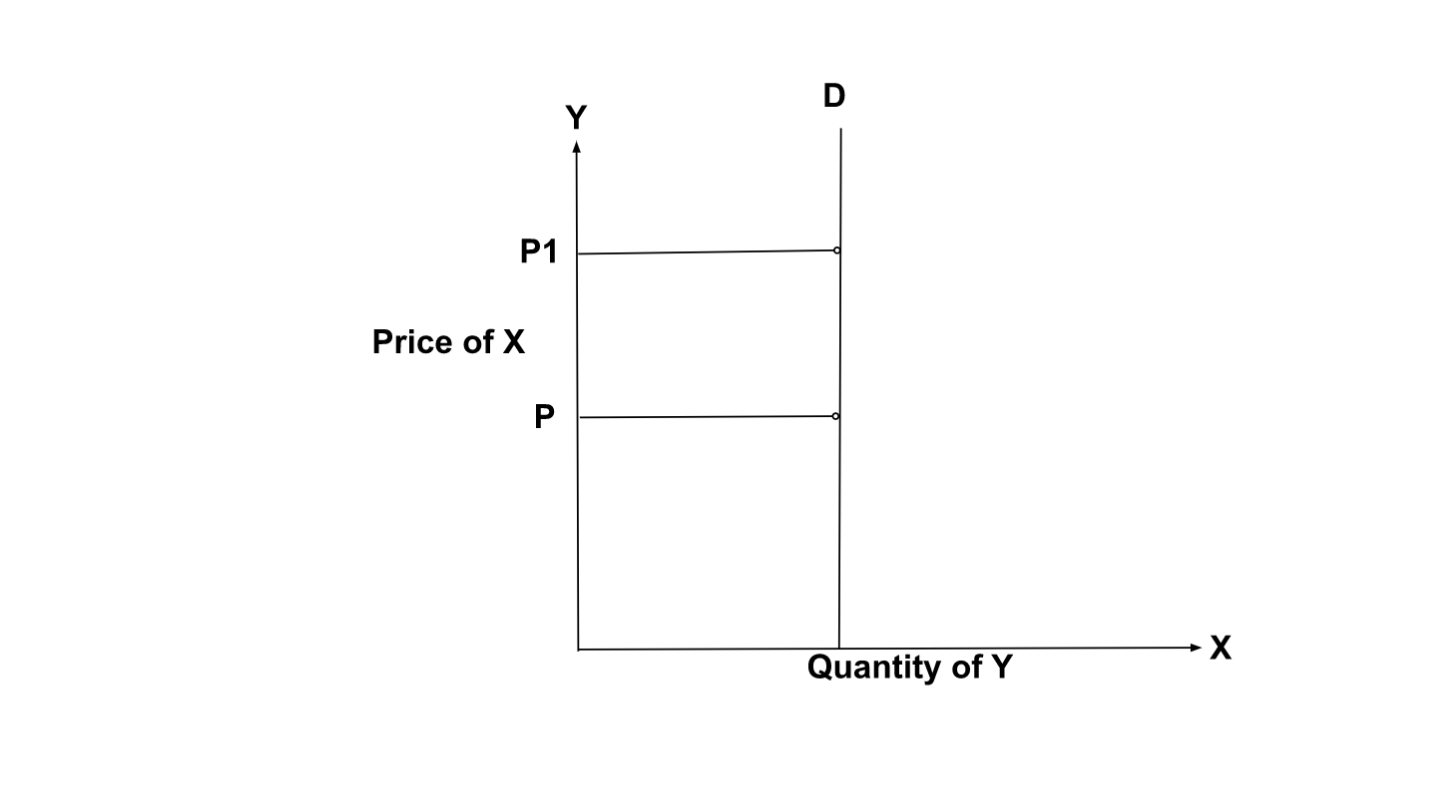

Case 3: Cross Elasticity of Unrelated Commodities

Cross elasticity of unrelated commodities is zero. A change in the price of commodity X will not affect the quantity demand of commodity Y when commodities are not related. Here, E = 0

Importance of Elasticity of Demand

- Elasticity is one of the important factors of defining the price of the commodity. If demand for a product is elastic, price is considerate and vice versa.

- Production function is highly dependent on elasticity of demand. Producers consider the production decision based on the elasticity of demand.

- Elasticity of demand is important for the factor of production. The elasticity of factors of productions lead to the bargain position of FOP.

- Elasticity of demand enables the government to decide on capital investment strategies regarding industries and other plants.

- This plays an important role in taxation and policies related to taxation. Government and policy makers consider the elasticity and behavior of goods for imposing tax on it. The nature of the commodity reflects the elasticity.

Reference