Credit Rating: History

With the growing market exposure, investors are concerned with two types of risks associated with their investments or potential ventures. The first risk associated is ‘business risk’ which is a macro risk factor which arises due to open market operation and business risk are uncertain. The second risk is ‘payment risk’ which is also a ‘default risk’. Business risk is exposure to uncertainty in economic value that cannot be market-to-market. Payment risk is exposure to the uncertainty of the debtor to pay the interest or principal. In order to manage such risks, investors, or any interested party establish and rank the credit credibility of a financial instrument, individual or company for better decision making.

Credit Rating can be simply defined as an data backed up opinion of rating agency which reflects the ability and willingness of the manager of debt instruments to fulfill its debt obligation when required. In simple terms, credit ratings ranks the issuer and debt instruments on the basis of their ability to fulfill the debt obligation. Credit Ratings are usually expressed in alphabetic and alphanumeric symbols.

Credit Ratings help to differentiate and rank various debt instruments and their issuer on the basis of their underlying credit quality. Ratings are very useful in understanding the quality of instruments or ability of the company and assist in informed investment decisions. Investors usually use credit ratings to optimise their risk-return trade-off. Credit ratings consider both the ability and willingness of an issuer to repay its debt in a timely manner.

A poor credit rating indicates that the company or government has a high risk of defaulting based on analysis and other long term prospects and vice-versa.

Credit Rating: Origin and History

The formal era of credit rating started back in 1841 in New York by Lewis Tappan where the world’s first mercantile credit rating agency ‘The Mercantile Agency’ was established. This agency evaluated the ability of merchants to pay their financial obligation. Later in 1859, Robert Dunn and John Bradstreet acquired The Mercantile Agency and named it Dun & Bradstreet. Dun & Bradstreet (D&B) are among front liners credit rating agencies. D&B endowed credit reports and sent reporters, on the field, to collect information about the business.

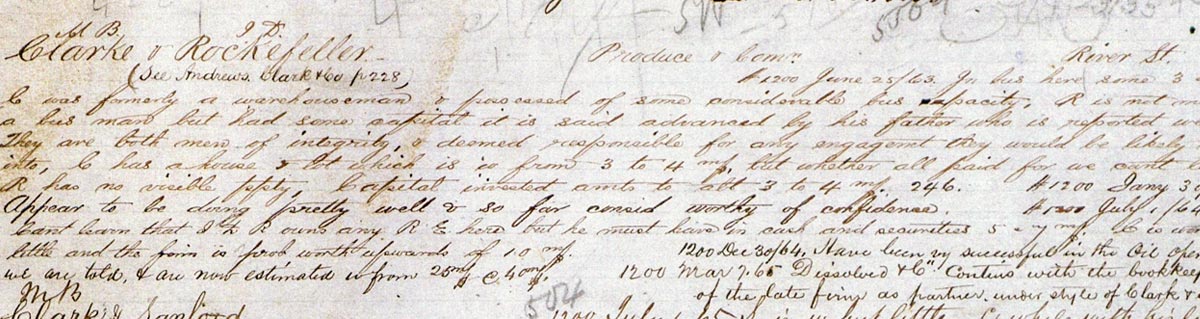

A note about M.B. Clark and John D. Rockefeller (1863) Source: HBR

This is a piece of approach to credit rating in 1863. John Moody in 1909 published a credit rating by making an opinion on creditworthiness of corporate debt issued by railroad companies. In 1916, Standard and Poor’s started publishing financial information and in 1924, a new rating scale was developed i.e. ‘AAA’ to ‘D’ rating which is still in practice.

The several market failure incidents all around the world, especially the U.S. market, have reflected the short-comings in credit ratings and also, at the same time, such incidents reflect the need for more solid credit ratings. U.S. market failure of 1929 sparked the importance of credit ratings as investors were more worried about the bond defaults and credit risks. Similarly, in 1970 the default of Penn Central Railroad of worth $82 million advocated for the need to have independent evaluation of credit risks available.

With the growing complexities in the business and business environment, the need for the credit rating agencies is also growing and credit rating agencies are working their best to rate the available instruments and companies, so that the market can regulate business and payment risk and investors can make informed decisions.

Credit Rating: Need

- Credit Rating makes the market aware about different instruments and their creditworthiness. It provides equal opportunities to all the investors while making a trade-off between risk and return.

- Credit Ratings provide confidence in the market. Markets are vulnerable to various financial and non- financial risks. Credit ratings assess the credit worthiness of instruments minimizing the risk and building confidence of investors in the market.

- Credit Ratings protect the small investors who wish to play safe. Investors take the credit ratings into consideration for risk-return trade-offs. Major investors adjust risk factors demanding higher return. Small investors or safe players can invest considering the credit ratings worrying less about risks. In absence of Credit Ratings, there are misjudged investment or promotion based investment.

- Credit Ratings provide information about the instruments and issuers. New savers are motivated to invest in business and instruments as credit ratings agencies have already done instrument and company assessment and reflected their position through credit ratings.

Credit Rating : Objectives

The primary objective of credit ratings is to provide quality and low cost information to investors and assist them in risk-return trade offs. Some of the others objectives are:

- To rate the debt instruments in order to build market confidence.

- To impose financial discipline on the borrowers.

- To guide the investors regarding making risk-return tradeoffs.

- To promote growth in the new issue market.

- To motivate new savers to invest in financial instruments.

- To facilitate in formulation of public guidelines on institutional investment

Credit Rating : Nature

Rating is based on information

Rating of financial instruments is solely based on the published information. This is the ground rule for any rating and also it is one of the limitations of rating systems. The quality of information available is reflected on the creditworthiness of the instrument. The assistance of the issuer regarding the insights about the instrument and performance of the company will help in precise valuation and rating of instruments. For such cooperation, rating agencies must not expose such confidential insights.

Rating by more than one agency

Rating has no standard form and parameter for credit rating and may vary from agency to agency. Same debt instruments can be rated differently by different credit rating agencies. The alphanumeric format for the same rating may also vary.

Many factors affecting rating

Credit rating doesn’t involve any particular mathematical formula. There is no standard format for calculating credit rating. Final rating considers various factors such as corporate strategy, expansion policies, operational consistency, quality of management, business environment, economic outlook etc. Along with it, some basic factors are financial and credit analysis.

Monitoring the already rates issues

Credit Rating is not a one time process. The parameter during the rating process may differ over the time. Credit rating agencies should regularly monitor the rated instruments and the factors associated with them. Agencies should regularly upgrade or downgrade the ratings as per new valuation. This will help investors to understand the potential of the instrument and make proper decisions.

Publication of Ratings

Rating process is different for different economies. In some economies, issuers request credit rating agencies to their instruments to encourage investment and in some economies, agencies independently rate various instruments with the corresponding available information. When rating is done as per request by the issue, the rating is published with the concern of the issue and if rating is conducted independently, agencies publish their work and make it available to investors.

Right of Appeal against assigned rating

If the issuer of the instrument is not happy with the rating then the issuer may request for review. In such a situation, the issuer will provide additional information evaluation which may result in an upgraded rate. The rating of the instrument is directly dependent on the information made available to the agencies or public. Unless the rating agency had overlooked critical information at the first stage chances of the rating being changed on appeal are rare.

Rating of rating agencies

Credit rating for the same instrument may vary from agency to agencies. The credibility of the ratings performed by the credit ratings depends on the creditworthiness of the rating agencies. The success of a rating agency is measured from the quality and consistency of past ratings, parameters and regularity in rating and eventually integrity of the agency.

Rating is for instrument and not for the issuer company

One of the most essential aspects of credit rating is that rating is for instruments not for the issuer company. Ratings on the two different instruments from the same company may be different. The rating doesn’t reflect on the issuing company. Yes, one might associate the issuer company with the nature of instruments it issues. Similarly, the obligation of the issuer company with the instrument may change with the nature of instrument issued.

Rating not applicable to equity shares

The name credit rating suggests that it is the rating of the debt instruments. Equity instruments don’t have obligations like debt instruments and equity investment is more likely a venture capital fund therefore, rating in equity is not applicable.

Credit rating vs Financial Analysis

It is one of the biggest misconceptions among investors that Credit Rating and Financial Analysis are the same. Credit Rating involves financial analysis but credit rating doesn’t only mean financial analysis. Credit rating involves multiple other factors that measure the qualitative and quantitative aspect of the instrument and the issuing company before final rating. Financial analysis is done for the issuer company. Credit analysis involves financial analysis to undertake the financial ability of the issuer to handle the instruments.

Credit Rating: Advantages

Benefits to Investors

Safe Investment Environment

Credit Ratings provide a prior approach to understanding the instrument and issuer company. Based on the advance information and ratings, investors invest on the desired instrument which qualifies their expectation. High rated instruments assure investors the instrument to be safe but return on investment is low and vice versa.

Recognition of Risk and Return

Credit rating is also the reflection of risk factors associated with the instrument. Higher rating signifies low risk of default and low rating reflects high chance of default. Credit ratings make work easier for investors to understand the worth of the instrument and issuer. Similarly, investors can assign and evaluate the risk-return factors associated with the instruments.

Freedom of Investment Decision

Credit Ratings is a publicly published document which reflects the potential of the instrument. Investors can rely upon these ratings for making their investment decision. Investors do not need to consider stock brokers, merchant bankers, portfolio managers, independent advisors etc. about the creditworthiness of the debt instrument with credit ratings. This is the freedom for investors in their investment decision.

Wider Choice of Investment

It is very essential for the issuer company to rate their debt instrument to increase the confidence of investors for their high rating issues. Similarly, there are multiple issues from multiple organizations and credit rating defines each issue and investors can choose the needed investment from this available variety of rated debt instruments.

Easy understanding of investment proposals

Credit rating agencies publish the final rating after considering various factors related to the particular instruments. The final rating published is denoted by alphabetical or alphanumeric symbols. Each symbol has some significance. Therefore, looking at these symbols, investors can easily understand the worth of the instruments.

Relief from botheration to know company

Credit rating is the final valuation of the debt instruments. The credit rating is alone capable of reflecting various information from its alphanumeric and alphabetic representation. Credit rating saves investors from hectic work company analysis and other valuations.

Advantages of continuous monitoring

Credit Rating is a continuous approach until the instrument is available in the market. Unlike other valuation. Credit rating is a continuous approach where the rating of instruments upgrade and downgrade subject to market factors.

Benefits to the Company

Easy to raise resources

Credit ratings measure multiple aspects of an instrument. A company with highly rated debt has probably the higher chances to raise funds from the market. The ratings of different instruments attract different sets of investors i.e. investment decision is informed and hence matching instruments with investors is easier.

Reduce the cost of borrowing

Credit Rating allows a match of risk-return factor associated with the instruments. Higher rated instruments means the chance of default is low or is secure investment and hence the return i.e interest on such instrument is lower. The issuer company will have enough ground to define market value of their instrument. A higher rated debt will have lower cost of borrowing.

Reduce the cost of public issues

A high rated instrument will have to face less challenges in attracting investors for raising funds. Also, credit rating will attract only those investors who are interested hece cost will be reduced as unwanted subscription while raising funds is minimized.

Rating reflects image

Credit rating is done for instruments but ratings can influence the image of the issuer as well. An issuer with high rated debt in its portfolio will definitely enjoy the goodwill and corporate image. The investors, customers, shareholders and creditors are assured about the issuers as the debt issued is highly rated. Everyone feels safe with their association with such an issuer.

Rating facilitates growth

Ratings attract the desired investors. A high rate debt instrument will have desired investors and raising of funds will not be an issue. This provides companies with an expansion strategy diversifying their business and operations. Highly rated companies will never feel shortage of funds as there are investors ready to invest on their highly rated goodwill.

Recognition of new/unknown companies

Rating is not preferred by all the issuers. As rating involves the disclosure of information, many new issuers prefer not giving this. A-rated issue in the market will have more credential than a normal public issue. Investors are sure about the credit rating as someone has conducted an analysis of such issues. Similarly, an unknown company gets some recognition in public issues due to credit rating.

References

1 thought on “What is CREDIT RATING?”